The True Cost of Solar: How Much Does Financing Add Up?

Understand your financial commitment when you switch to solar energy.

Are you thinking about solar panels but worried about the upfront cost? Financing helps many homeowners get solar.

Understand solar loans, interest rates, and tax credits. This helps you make a smart long-term investment.

Avoid hidden fees or complex terms. We explain all you need to know about the price of solar financing.

Many homeowners consider solar energy. It offers environmental benefits, energy independence, and long-term savings on utility bills. The initial investment seems difficult. This makes many people ask: how much does financing solar cost?

This guide explains the financial aspects of going solar. We examine different financing options. We explain interest rates, tax credits, and incentives. We also show important rules that affect your total cost. You will understand the true price and make a good decision for your home.

Table of Contents

- The Real Cost of Going Solar: More Than Just Panels?

- Understand Solar Loans: APR, Terms, and Your Credit Score

- Get Savings: Tax Credits, Rebates, and Other Incentives

- Beyond the Loan: Understanding Long-Term Financial Implications

- What this means for you

- Risks, trade-offs, and blind spots

- Main points

The Real Cost of Going Solar: More Than Just Panels?

Is the initial price tag the only figure you should be considering for your solar investment?

When you consider installing solar panels, you probably think of the equipment price first. The true cost of a solar system involves more than the panels. It includes factors like inverters, mounting hardware, wiring, installation labor, permitting fees, and electrical panel upgrades.

Understand these parts first. This helps answer what solar financing truly means. The gross cost is the total price before incentives or financing changes. The net cost is the price after considering tax credits and rebates. Financing helps homeowners spread this investment over time. This makes solar energy available without a large upfront payment.

Many people cannot pay cash upfront. Financing solutions help. They change a big cost into smaller monthly payments. Assess the system cost. Also, assess the total cost of ownership over its life. This includes interest paid on the financed amount.

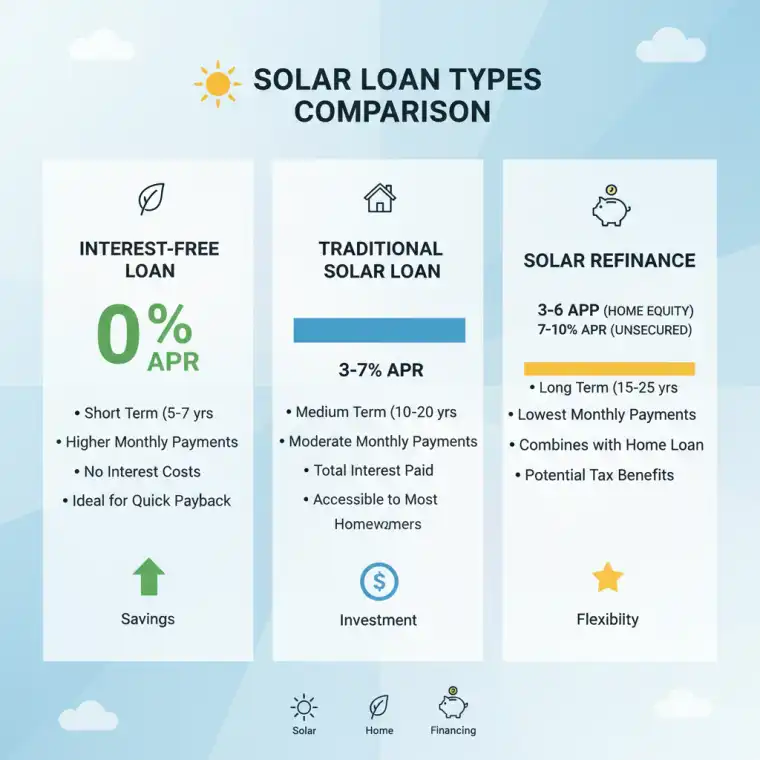

Understand Solar Loans: APR, Terms, and Your Credit Score

How do you pick the right solar loan without getting confused by financial terms?

Solar loans seem complex. Understand the key terms. Most homeowners choose solar loans. These loans are secured, like a home equity loan, or unsecured personal loans. People often discuss Power Purchase Agreements (PPAs) and leases with financing. You must differentiate them. With a PPA or lease, you do not own the system. You pay for the electricity it makes or lease the equipment. True financing means you own the system and repay a loan.

The Annual Percentage Rate (APR) is an important number. It shows the true cost of borrowing. This includes interest and other fees. Loan terms usually range from 10 to 25 years. They affect your monthly payment and total interest paid. Your credit score is very important in getting an interest rate. Higher scores give you better terms.

Many lenders have specific qualification rules. For example, the 33% rule often means your debt-to-income (DTI) ratio. Your total monthly debt payments should not go over 33% of your gross monthly income. A 20% rule often means a down payment for certain loan types. Many solar loans offer $0 down options. Discussions on platforms like Reddit show confusion about these numbers. Users often ask "how much does financing solar panels cost reddit" and want clear details.

Compare multiple loan offers. Examine more than the monthly payment. Also look at the total interest over the loan term. Ask lenders for a clear breakdown of all costs and fees for your solar loan.

Get Savings: Tax Credits, Rebates, and Other Incentives

Are there hidden financial gains that greatly reduce your out-of-pocket expenses?

Beyond the loan, various incentives greatly reduce your solar investment's overall cost. This makes solar financing more appealing. The most well-known is the federal Solar Investment Tax Credit (ITC). It offers a large percentage of your system's cost as a tax credit. This is not a deduction. It is a direct reduction in the tax you owe.

Many states and local municipalities offer their own rebates, grants, or property tax exemptions for solar installations. This is in addition to the ITC. Some regions also have Solar Renewable Energy Credits (SRECs). You earn credits for the clean electricity your system makes and sell them on a market. These programs encourage solar energy use. They greatly lower your net financial commitment.

Factor these incentives into your financial calculations. A loan covers the gross cost. These savings reduce what you pay out-of-pocket. Sometimes they make a smaller loan amount or faster repayment possible. Always research the specific incentives in your area. They vary widely and change over time.

Beyond the Loan: Understanding Long-Term Financial Implications

What happens after the installation—are there ongoing costs or future opportunities to consider?

Your financial commitment with solar panels continues after installation and paying off the loan. Long-term issues affect your overall costs and savings. Solar panels need minimal maintenance. Occasional cleaning is sometimes necessary. Inverters usually need replacement after 10-15 years. Plan to budget for these operational costs.

Consider insurance. Your homeowner's insurance policy needs updating to cover the new solar equipment. A positive aspect is that solar panels greatly increase your home's value. You often see this benefit when selling the property. The biggest long-term financial benefit comes from lower or no monthly electricity bills. This balances the cost of financing over time.

You might refinance your solar loan in the future. This brings more savings, especially if interest rates drop or your credit score improves. Monitor your system's performance. Understand its ongoing financial impact. This helps you get the most from your investment.

What this means for you

With this information, how do you confidently determine your path to solar energy?

Making an informed decision about financing solar panels requires you to carefully consider your personal financial situation and energy goals. Start by getting multiple quotes for solar system installation. At the same time, examine different financing options from various lenders. Compare monthly payments. Also, compare the total cost of ownership over the loan term. Include all interest and fees.

Pay close attention to tax credits and incentives in your area. These greatly reduce your net cost. Ask detailed questions about loan terms, prepayment penalties, and other contract clauses. Consider the long-term benefits of lower electricity bills and increased home value. Weigh these against financing costs and possible maintenance.

A well-researched and strategically financed solar system is a smart investment for your home and the environment. For residents in specific areas, understanding local installers and regulations is also important. For example, those in the Houston area benefit from looking at local options, like those detailed at Solar Panel Installation in Houston. This helps you get the best local advice and service.

Risks, trade-offs, and blind spots

What are the potential problems and less obvious factors you know about before signing the contract?

Solar financing offers many benefits. It is important to know about potential risks and trade-offs. One blind spot sometimes involves predatory lenders or aggressive sales tactics. Always work with reputable companies. Fully understand every clause in your loan agreement. Some loans place a lien on your property. This impacts future refinancing or selling your home.

Interest rate changes affect your long-term costs, though they are more common with variable-rate loans. Understand the specifics of tax credits. They are highly beneficial, but they are not guaranteed income. They depend on your individual tax liability. Future changes in energy policies or net metering rules also affect your solar investment's financial returns.

A lower monthly payment often means a longer loan term. This also means paying more interest overall. Weigh these factors carefully. Ensure your financing choice matches your financial comfort and long-term goals. Be diligent and critical. These are your best ways to prevent unforeseen problems.

Main points

Need a quick recap? What are the absolute essentials to remember about solar financing?

- Solar financing makes renewable energy available by spreading the initial investment over time.

- Compare loan types, APRs, and terms from many lenders. Find the best fit for your credit score and finances.

- Federal tax credits (like the ITC), state rebates, and local incentives greatly reduce your solar system's net cost.

- Know specific financial rules. These include debt-to-income ratios (e.g., 33%) and down payment requirements (e.g., 20%).

- Consider long-term effects. These include possible maintenance costs, increased home value, and utility bill savings.

- Review all contract details fully. Avoid hidden fees, predatory terms, or liens on your property.

Understanding what solar financing truly means is the first step toward a sustainable future for your home. Be informed about financial options, incentives, and long-term impacts. Then you make a confident decision. This benefits you financially and helps the planet for years.