How Much Does Financing Solar Panels Really Cost?

Understand the True Financial Commitment of Going Solar

Considering solar panels but worried about the upfront investment? Understanding the true cost of financing is your first step.

Forget vague estimates. We break down every financial aspect. Learn about interest rates, hidden fees, and incentives.

Learn how to navigate loans, leases, and PPAs. Find the most affordable path to clean energy for your home.

Going solar is an important decision. It offers long-term savings and environmental benefits. Many homeowners concern themselves with this: how much does financing solar panels cost? It is more than the sticker price. It involves a detailed understanding of loan structures, interest rates, lease agreements, and power purchase agreements (PPAs).

This guide explains the financial aspects of solar energy. It helps you find potential expenses, incentives, and financial rules you need to consider before investing. You will have a clear picture of expectations and how to make the best financial choice for your solar plan.

Quick navigation

- Understanding Solar Financing: Loans, Leases, and PPAs

- Deconstructing the Costs: Interest Rates, Fees, and Hidden Charges

- Navigating Incentives: Tax Credits, Rebates, and SRECs

- Applying the Affordability Rule to Solar Investments

- What This Means For You: Making an Informed Decision

- Risks, Trade-Offs, and Blind Spots in Solar Financing

- Main Points: Your Path to Affordable Solar

Understanding Solar Financing: Loans, Leases, and PPAs

You are ready to go solar, but which financing path should you choose? Exploring the various ways to finance solar panels is important. Each option has financial implications and benefits.

You have three main routes: solar loans, solar leases, and Power Purchase Agreements (PPAs). Each offers different ownership levels, upfront costs, and long-term savings. Understand these distinctions. This is the first step to determine your true financing cost.

Solar Loans: The Path to Ownership

A solar loan works like any other home improvement loan. You borrow money from a bank or a specialized solar lender to pay the upfront cost of your system. Once repaid, you own the panels.

- Pros: Full ownership, eligibility for tax credits and incentives, increased home value.

- Cons: Requires a good credit score, monthly payments with interest, responsibility for maintenance.

The total cost includes the principal amount, interest over the loan term, and any related fees. Loans are either secured, using your home as collateral, or unsecured, with higher interest rates and no collateral.

Solar Leases: Paying for Use, Not Ownership

With a solar lease, you rent the solar panel system from a third-party company. You pay a fixed monthly fee. You use the electricity generated by the panels.

- Pros: No upfront costs, predictable monthly payments, maintenance typically handled by the leasing company.

- Cons: No ownership, not eligible for tax credits or incentives, potential complications when selling your home.

The cost is mainly your monthly lease payment. It might increase over the contract term. You save on your utility bill, even without ownership.

Power Purchase Agreements (PPAs): Paying for Power

A PPA is similar to a lease; a third-party owns and maintains the system on your roof. You purchase the electricity generated by the panels at a set rate per kilowatt-hour (kWh) instead of a fixed monthly payment for the system.

- Pros: Zero upfront cost, predictable electricity rates, no maintenance responsibility.

- Cons: No ownership, no eligibility for tax credits, rates might increase slightly over time.

The cost is directly based on your energy consumption from the solar panels. If the solar system produces more, you pay more to the PPA provider. Your utility bill savings still make it a good value.

For more information on common misconceptions, read this article: Residential Solar Financing Myths Debunked.

Deconstructing the Costs: Interest Rates, Fees, and Hidden Charges

Are you aware of every dollar you spend when financing solar panels? Many people only focus on the monthly payment. However, the real cost is often hidden.

Beyond the loan's principal amount or the advertised lease payment, other financial components make up the overall cost of your solar investment. These include interest rates, various fees, and less obvious charges that increase your total cost much.

Understanding Interest Rates

For solar loans, the interest rate is the most important factor for your total repayment. A difference of just a few percentage points can become thousands of dollars over a 15-20 year loan term. Factors affecting your interest rate include your credit score, the loan term, and the lender's current offerings.

It is important to shop around and compare APRs (Annual Percentage Rates) from multiple lenders. Some solar companies offer promotional rates. These come with specific terms or a higher dealer fee built into the system price.

Unveiling Loan and Administrative Fees

When you get a solar loan, prepare for various fees:

- Origination Fees: A charge by the lender for processing the loan, usually a percentage of the loan amount.

- Dealer Fees (or Discount Fees): Often included in zero-interest or low-interest rate loans. The solar installer pays a fee to the lender to buy down the interest rate. This then passes on to you in the system's total price. This increases the quoted system price much.

- Closing Costs: Similar to a mortgage, these cover legal, appraisal, and administrative expenses.

- Prepayment Penalties: Some loans charge a fee if you pay off your loan early.

Always ask for a full breakdown of all fees before signing any agreement. Transparency avoids surprises.

Hidden Costs and What to Look For

Other factors add to your total financial cost, beyond explicit fees:

- Escalator Clauses (Leases/PPAs): Some agreements include annual rate increases, typically 1-3%. This adds up over a 20-25 year contract.

- Inverter Replacement: Inverters have a shorter lifespan than panels (10-15 years). If you own the system, you are responsible for this cost.

- Maintenance and Cleaning: Solar panels require minimal maintenance. Occasional cleaning might be necessary, especially in dusty areas. Repair costs for unforeseen damage fall to the owner.

- Insurance Premiums: Your homeowner's insurance might increase to cover the added value of the solar system.

A full understanding of these potential costs prepares you for the financial aspects of solar ownership or usage. The world uses much solar energy. You must make informed decisions.

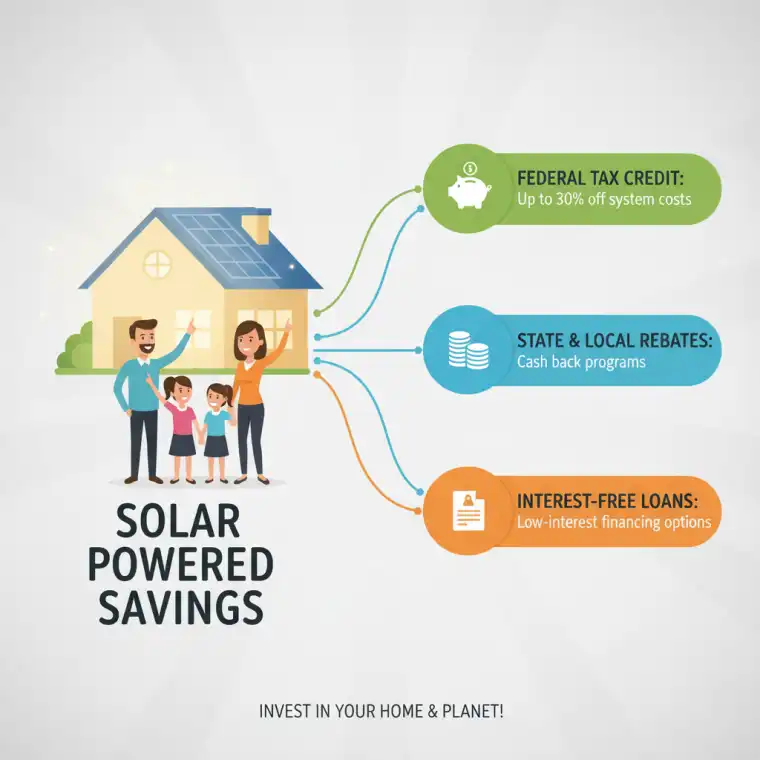

Navigating Incentives: Tax Credits, Rebates, and SRECs

Can financial incentives change your view of solar panel affordability? Yes. One of the best aspects of going solar is the available financial incentives. These reduce your overall financing costs much.

These incentives include federal tax credits, state and local rebates, and Solar Renewable Energy Certificates (SRECs). They encourage renewable energy use. Using them well makes a large difference in your long-term savings.

The Federal Solar Investment Tax Credit (ITC)

The most important incentive is the federal Solar Investment Tax Credit (ITC). This lets homeowners deduct a percentage of the cost of installing a solar energy system from their federal taxes.

- Current Rate: As of the Inflation Reduction Act of 2022, the ITC is set at 30% for systems installed through 2032.

- Eligibility: Applies to owned systems (purchased outright or financed with a loan), not leased systems or PPAs.

- Impact: This credit directly reduces your tax liability. It lowers the net cost of your system much.

It is important to understand that it is a credit, not a refund. You need enough tax liability to claim the full amount. Unused credit can be rolled over to subsequent tax years.

State and Local Rebates

Many states, counties, and even cities offer their own incentive programs. These range from direct rebates that lower the upfront purchase price to property tax exemptions for the added value of solar panels.

- Examples: Some states offer performance-based incentives (PBIs) where you get paid for the electricity your system generates.

- Check Local Programs: Programs vary widely by location. Check with your state energy office, local utility provider, or a reputable solar installer for details specific to your area.

Solar Renewable Energy Certificates (SRECs)

SRECs are a market-based incentive available in certain states. When your solar panels generate electricity, you earn one SREC for every megawatt-hour (MWh) of power produced. You sell these SRECs on a market to utility companies that need to meet renewable energy mandates.

- Market Value: The price of SRECs fluctuates based on supply and demand within your state's market.

- Passive Income: Selling SRECs provides a valuable stream of passive income. It further offsets your solar financing costs.

Combining these incentives greatly improves the return on investment for your solar system. It makes it more affordable than the initial sticker price suggests. Factor these into your financial calculations.

Applying the Affordability Rule to Solar Investments

How do you gauge if a solar financing plan is within your budget without overspending? Like any major home investment, financial principles guide your decision-making. They help you determine if a solar financing option is affordable for you.

Understanding and applying concepts like the "33% rule" or "20% rule" – commonly used in housing and debt management – provide a framework to assess the true financial commitment of your solar panels.

The 33% Rule for Overall Debt

The 33% rule, often applied to housing costs, suggests that your total housing expenses (mortgage, property taxes, insurance, utilities) not exceed 33% of your gross monthly income. When considering solar, your new "utility" cost, even if a loan payment, adds to this overall housing expense.

- Application: If your solar loan payment, combined with your remaining utility bill, pushes your total housing costs much over this threshold, it indicates an overextension.

- Context: This rule is a guideline. A solar loan might increase a monthly payment. It often replaces or greatly reduces a pre-existing utility bill. Calculate the net impact carefully.

The 20% Rule for Discretionary Debt

The 20% rule suggests that your total consumer debt payments (excluding mortgage) not exceed 20% of your net monthly income. A solar loan is a home improvement. If it is an installment loan, it falls under this category depending on the lender.

- Consideration: If your current consumer debt is high, adding a solar loan payment strains your budget. This is true even if it saves you money on electricity.

- Prioritize: Assess your current debt load and repayment capacity. View a solar loan as an investment that *reduces* overall household expenses over time. It should not add more debt.

Calculating Net Monthly Impact

The best way to apply these rules to solar financing is to calculate the net monthly impact. Compare your current average utility bill to your new solar loan/lease/PPA payment *minus* the new, reduced utility bill. If the net monthly expense increases much, consider it carefully against your income and other financial obligations.

Perform a cash flow analysis to ensure the new financial commitment fits your budget comfortably. Respect your personal affordability limits. Saving money long-term should not mean struggling short-term. Need help with installation costs? Find local information here: Solar Panel Installation in Houston.

What This Means For You: Making an Informed Decision

After understanding loans, leases, PPAs, hidden fees, and incentives, how do you make a confident decision for your home with this information? The journey to solar energy requires careful thought about financial aspects. The 'best' financing option is not universal. It is personal. It depends on your financial situation, goals, and risk tolerance.

Consider these points when making your final decision:

Assess Your Financial Health and Goals

- Credit Score: A strong credit score gives you the best loan terms and lowest interest rates.

- Upfront Capital: Do you have savings for a down payment or outright purchase? This reduces interest costs much.

- Ownership Preference: Do you want to own your system and maximize long-term savings and property value? Or do you prefer energy production without ownership and no hassle?

- Tax Appetite: Can you fully use the federal ITC? If not, a loan might still offer benefits. However, its immediate financial appeal is reduced.

Compare All Offers Diligently

Do not settle for the first quote. Get multiple quotes from different installers and lenders. Compare the system price, the total cost of ownership over 20-25 years for loans, and the total payments over the contract term for leases and PPAs.

- Look Beyond Monthly Payments: Focus on the total principal + interest, and any hidden fees.

- Factor in Incentives: Consider how federal, state, and local incentives reduce your *net* cost.

Prioritize Long-Term Value

Low monthly payments are appealing. Understand the long-term implications. A slightly higher monthly payment for a loan leads to much greater overall savings and ownership benefits compared to a lease or PPA with escalator clauses.

Your informed decision creates a more sustainable future and large savings. Ask the right questions. Demand full transparency from your solar provider.

Risks, Trade-Offs, and Blind Spots in Solar Financing

Even with careful planning, are there financial problems or overlooked aspects that impact your solar investment? Every important financial decision has risks. Solar panel financing is not different. The benefits are clear, but it is important to know potential trade-offs and common blind spots that affect your long-term satisfaction and financial outcome.

Understanding these challenges upfront allows you to address them or make better decisions.

Interest Rate Fluctuations and Market Changes

If you choose an adjustable-rate solar loan (less common but possible), your monthly payments increase if interest rates rise. Even for fixed-rate loans, a poor market environment when you secure the loan means higher rates than you gotten otherwise.

- Trade-off: Waiting for better rates might mean missing out on current incentives or higher utility bill savings.

- Mitigation: Prioritize fixed-rate loans for predictable payments.

Resale Value and Transferability

Owned solar systems generally increase home value. Leased systems or PPAs complicate home sales. Buyers hesitate to take on an existing agreement or face credit checks by the solar provider.

- Trade-off: No upfront cost offers convenience. This trades for potential complexities during resale.

- Mitigation: Review the transfer clauses in lease/PPA agreements carefully.

Technological Obsolescence and System Performance

Solar technology is always changing. Your panels last decades, but newer, more efficient models emerge. System performance varies based on weather, shading, and degradation.

- Blind Spot: Overestimating energy production or underestimating panel degradation over 25 years.

- Mitigation: Get production guarantees from installers, monitor system performance, and factor in a conservative degradation rate (e.g., 0.5% per year).

The "Dealer Fee" Illusion

Many "zero-interest" or "low-interest" solar loans include a large dealer fee. This fee rolls into the total system price. You pay interest upfront. It comes disguised as a higher system cost. This inflates the amount you need to borrow and the overall cost, even if the APR looks low.

- Blind Spot: Do not realize that a higher system price compensates for a lower interest rate. This reduces the net savings from the federal ITC, which bases itself on the system cost.

- Mitigation: Ask for the cash price of the system versus the financed price. Compare the total amount paid under both scenarios.

By being aware of these problems, you approach solar financing clearly. Negotiate terms to protect your interests.

Main Points: Your Path to Affordable Solar

Ready to find affordable solar for your home? Financing solar panels seems daunting. But with the right knowledge, you make a choice that powers your home and saves money for years.

Here is a recap of essential points to guide your solar financing:

- Explore All Options: Understand the differences between solar loans (ownership, incentives), leases (no upfront cost, no ownership), and Power Purchase Agreements (PPAs, pay for power, no ownership).

- Understand Costs: Do not just look at monthly payments. Account for interest rates, origination fees, dealer fees, and hidden costs. These include escalator clauses or future inverter replacements.

- Maximize Incentives: Leverage the federal Solar Investment Tax Credit (ITC). Investigate state/local rebates and SRECs to reduce your net cost much.

- Apply Affordability Rules: Use financial guidelines like the 33% or 20% rules. Assess if the net monthly cost of solar fits your budget comfortably after factoring in utility bill savings.

- Compare and Negotiate: Get multiple quotes. Ask for the cash price versus the financed price. Be transparent about your financial goals. Ask for all fee breakdowns.

- Be Aware of Risks: Understand issues like transferability if you move. Understand the impact of dealer fees on your system's total cost and long-term performance expectations.

By researching carefully, comparing offers, and understanding all financial parts, you invest confidently in solar energy. This ensures a sustainable and financially sound future for your home. Your path to energy independence starts with a smart financing decision.