Solar Financing Loans vs. Lease vs. Cash: Navigating Your Best Path to Renewable Energy

A comprehensive guide to understanding the financial implications, benefits, and drawbacks of going solar with loans, leases, or outright cash.

Considering solar panels for your home is a monumental decision, promising environmental benefits and long-term savings, but the financial path can feel like a complex maze. Will you own your power outright, or will you simply rent the sunshine?

The options for going solar are more diverse than ever, from significant upfront investments to zero-down possibilities. Yet, each choice carries unique financial implications that could dramatically alter your long-term gains.

Realizing the full value of solar energy for your property depends less on the panels themselves and more on how you choose to pay for them. Are you truly prepared to make the most informed decision for your financial future and energy independence? Understanding these options is not just about saving money; it's about shaping your long-term financial landscape and contributing to a sustainable future.

The allure of solar energy is undeniable: reduced electricity bills, a smaller carbon footprint, and enhanced energy independence. Yet, for many homeowners, the initial investment can seem daunting. Navigating the world of solar financing can be as complex as understanding the technology itself. With options like solar financing loans vs. lease vs. cash, prospective solar owners are often faced with a crucial decision that will impact their financial health for decades. This comparison isn't merely about cost; it's about ownership, long-term savings, eligibility for incentives, and the overall value proposition for your home. It's about empowering homeowners to make a conscious choice that aligns with both their environmental aspirations and financial realities, avoiding common pitfalls that can diminish the promised benefits.

This comprehensive guide aims to clarify these choices, offering an in-depth look into the financial implications, distinct benefits, and potential drawbacks of each method. We will explore how different financing options impact your bottom line, property value, and eligibility for valuable tax credits and rebates. By dissecting each approach, from outright cash purchases to various loan structures and leasing arrangements, you'll gain the clarity needed to determine which solar financing path aligns best with your specific financial situation, ownership goals, and even your geographic location, like in bustling California or sunny Florida, helping you make a truly informed decision. We will delve into how each method impacts not only your wallet but also your property's appeal and your ability to adapt to future energy needs.

Quick navigation

The Foundations of Solar Investment: Ownership vs. Access

Before diving into the specifics of loans, leases, or cash, it's vital to grasp the fundamental distinction that underpins all solar financing decisions: do you want to own your solar power system, or do you simply want to access the electricity it produces? This core question will largely dictate which financing option is most suitable for you, affecting everything from your upfront investment to your eligibility for tax benefits and the overall return on your solar investment over decades.

When you choose to own your solar system, either through a cash purchase or a solar loan, you become the legal proprietor of the equipment installed on your roof. This means you gain direct access to all available financial incentives, such as federal tax credits, state rebates, and net metering programs, which can significantly reduce the overall cost and improve your return on investment. Ownership also gives you complete control over your system's performance, maintenance, and future upgrades. Furthermore, an owned solar system often increases your home's property value, making it a tangible asset that contributes significantly to your net worth.

Conversely, a solar lease or a Power Purchase Agreement (PPA) structure means you do not own the solar panels. Instead, a third-party company, typically the solar installer, retains ownership. You essentially pay them a fixed monthly fee (for a lease) or a per-kilowatt-hour rate for the electricity generated (for a PPA). While this eliminates upfront costs and maintenance responsibilities, it also means the leasing company reaps the benefits of most financial incentives, and you only benefit from the reduced electricity bill. This fundamental difference in ownership dictates who benefits from the system's long-term value. Is your primary goal maximizing financial return and control, or is it simply minimizing upfront investment and hassle? This fundamental choice is the compass for your solar journey.

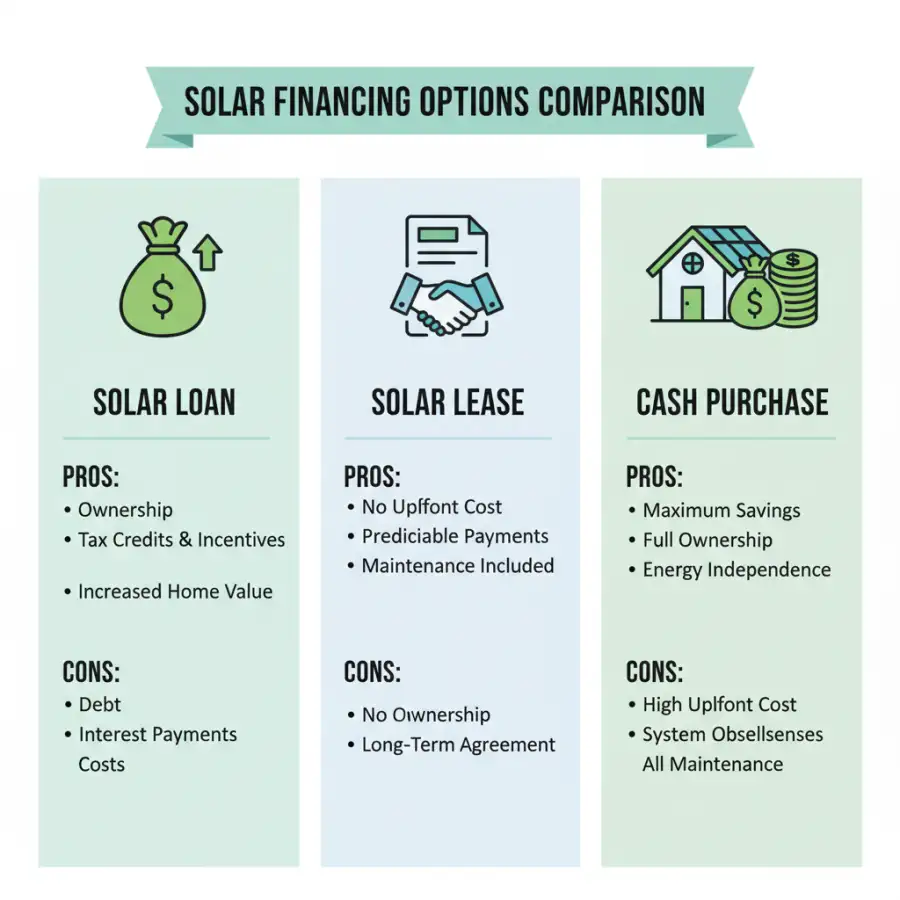

Solar Loans: Ownership on a Payment Plan

For many homeowners, a solar loan strikes a compelling balance between outright ownership and manageable payments. When you opt for a solar loan, you finance the purchase and installation of your system, much like buying a car or funding a home improvement. The crucial advantage here is that you own the solar panels from day one. This makes you eligible for the substantial federal solar tax credit (Investment Tax Credit, ITC), which can cover a significant percentage of your system's cost, along with any state or local incentives available in your area, such as SRECs (Solar Renewable Energy Credits) or performance-based incentives.

Solar loans come in various forms, including secured loans (like a home equity loan or HELOC) or unsecured personal loans specifically for solar. Secured loans often offer lower interest rates due to the collateral, but they put your home at risk if you default. Unsecured loans typically have higher interest rates but carry no collateral, offering a less risky proposition for your home equity but potentially a higher monthly payment. Loan terms usually range from 10 to 20 years, with fixed monthly payments, though some lenders may offer shorter or longer terms. It's vital to shop around for competitive interest rates and understand all fees associated with the loan, including origination fees, application fees, or prepayment penalties, as these can add significantly to the overall cost.

The financial benefit of a loan often materializes as your monthly loan payment is offset by (or ideally, less than) your reduced electricity bill. Over the life of the system, after the loan is repaid, you enjoy free electricity for the remaining lifespan of your panels, which can be 25-30 years or more. This path allows you to build equity in your system, potentially increasing your home's value and offering a clear, quantifiable return on investment. However, your credit score will play a significant role in the interest rate you qualify for, directly impacting the total cost of your system over time, making a strong credit profile highly advantageous. Are you comfortable with a monthly payment and managing debt in exchange for eventual ownership and maximum long-term savings?

Solar Leases and PPAs: The 'No Upfront Cost' Appeal

For homeowners keen on going solar without any upfront cash outlay, solar leases and Power Purchase Agreements (PPAs) present an attractive alternative. These options are often marketed as "zero-down solar," appealing to those who lack the capital for a cash purchase or the creditworthiness for a favorable loan. However, it's crucial to understand that with a lease or PPA, you do not own the solar energy system; you are essentially paying for the electricity it generates, or renting the equipment.

In a solar lease, you essentially rent the solar panels from a third-party company (the lessor) for a fixed monthly payment, typically over a 20- to 25-year term. The lessor owns, installs, monitors, and maintains the system. Your benefit comes from paying a lower monthly lease payment than what you would have paid for utility electricity, resulting in immediate savings. Similarly, a Power Purchase Agreement (PPA) also involves a third party owning and maintaining the system, but instead of a fixed monthly payment, you agree to purchase the electricity generated by the panels at a predetermined, per-kilowatt-hour rate, usually lower than your utility's rate, often with a slight annual escalator. Both models transfer maintenance responsibilities, performance guarantees, and the benefit of most incentives (like the federal ITC) to the third-party owner, simplifying the solar experience for the homeowner.

The primary advantage of leases and PPAs is precisely their "no upfront cost" nature, making solar accessible to a broader range of homeowners. The leasing company handles all installation and maintenance, removing any homeowner burden. However, the major drawback is the lack of ownership; you do not gain the tax credits or other financial incentives, and the overall long-term savings are generally lower than with ownership models. Furthermore, selling a home with a solar lease or PPA can sometimes complicate the transaction, as the new homeowner must qualify and agree to assume the agreement, which might deter potential buyers. It's essential to scrutinize the contract terms carefully, including any escalator clauses that might increase your monthly payments or per-kWh rate over time (e.g., 2-3% annually), potentially eroding your savings over two decades. While the appeal of immediate savings is strong, are you truly comfortable giving up ownership and the associated long-term financial benefits for the sake of convenience and zero upfront investment, and potentially complicating a future home sale?

The Cash Advantage: Maximum Savings and Control

For homeowners with the financial means, an outright cash purchase of a solar energy system almost invariably offers the highest return on investment and the greatest long-term savings. This method completely bypasses interest payments, financing fees, and lease terms, putting you in full control of your solar asset from the moment of installation, ensuring maximum long-term value capture. This approach is often considered the gold standard for maximizing the financial benefits of going solar.

With a cash purchase, you are the undisputed owner of the system, which means you are fully eligible for all available financial incentives. This includes the significant federal solar Investment Tax Credit (ITC), which currently offers a substantial tax credit on the total cost of your system, along with potential state or local rebates that can further reduce your out-of-pocket expenses. In addition, you retain full entitlement to any state or local rebates, grants, and renewable energy credits (RECs) that may be available in your area, providing multiple layers of financial benefit.

Beyond incentives, cash buyers benefit from immediate and maximal reductions in their monthly electricity bills, effectively turning a variable utility expense into a fixed, one-time investment. After the initial outlay, your energy production is essentially free for the lifespan of the panels, which can easily exceed 25 years. This leads to the lowest lifetime cost of electricity and the fastest payback period compared to loans or leases. Moreover, owning your system outright offers complete flexibility for future upgrades, maintenance choices, and potential battery storage integration, giving you ultimate autonomy over your energy production. An owned system also adds tangible value to your property, a key consideration for homeowners looking to boost their home's market appeal and secure a higher resale price. This approach represents the pinnacle of control and financial benefit in the solar journey, transforming your home into a self-sufficient power generator, offering unparalleled energy independence. However, is the initial significant investment feasible for your current financial situation, even with the promise of unparalleled long-term gains and complete control?

What this means for you

Choosing the right solar financing option isn't a one-size-fits-all decision; it depends heavily on your individual financial health, ownership aspirations, and even where you live. Understanding the nuances of solar financing loans vs. lease vs. cash is crucial for making a choice that truly benefits you, ensuring your investment serves your financial and environmental goals effectively.

If you have substantial savings and want to maximize your long-term return and control, a **cash purchase** is likely your best bet. You’ll capture all available incentives, avoid interest payments, and see the fastest payback period. This option is particularly compelling in states like California or Florida, where high electricity rates and strong solar irradiance mean significant savings over time. However, it requires a considerable upfront investment.

For those who want ownership and access to incentives but prefer not to pay a large sum upfront, a **solar loan** offers an excellent compromise. Loans allow you to spread the cost over many years, potentially with monthly payments that are lower than your current electricity bill. Your credit score will dictate your interest rate, so strong credit is a definite advantage, allowing you access to the most favorable terms. Be sure to consider your total cost over the loan term and factor in the federal tax credit when evaluating affordability, as it can significantly reduce your net investment. This approach is often ideal for homeowners who want to boost their home’s value and benefit from ongoing tax incentives, as discussed in guides to residential solar panel installation, without the large upfront capital.

If minimizing upfront costs and avoiding maintenance responsibilities are your top priorities, and you are comfortable foregoing ownership and most incentives, a **solar lease or PPA** could be suitable. These options provide immediate savings on your electricity bill with little to no money down. They can be a good entry point into solar, especially if you plan to move within a few years or have limited access to financing, but understanding the lease transfer process is vital. However, remember you won't own the system or claim the federal tax credit, and your overall savings might be less compared to ownership. This is a common choice for those prioritizing simplicity and immediate budget relief, but it requires careful review of the long-term contract implications. Ultimately, your choice should align with your long-term financial goals and your comfort level with different levels of financial commitment and system control. Are your current financial circumstances dictating your energy future, or can you strategically choose a path that maximizes your long-term gains and minimizes future complications?

Risks, trade-offs, and blind spots

While the promise of solar energy is bright, each financing method comes with its own set of potential pitfalls, trade-offs, and details that are often overlooked. A thorough understanding of these "blind spots" is essential for making a truly informed decision, preventing costly surprises down the road and ensuring the solar dream doesn't become a financial burden.

For **solar loans**, the primary risk lies in the interest rate and loan terms. A high-interest rate can significantly erode your savings, making the total cost of your system much higher than expected. Some loans may also have balloon payments or variable rates, which can introduce significant financial uncertainty over time. It's critical to read the fine print, understand all fees, and consider how a long-term loan might impact your debt-to-income ratio or future refinancing options, as well as your overall financial flexibility. Not taking full advantage of the federal tax credit by either not qualifying or not claiming it can also drastically alter your financial projections, making the "solar financing loans vs. lease vs. cash calculator" essential to run to see the true cost.

**Solar leases and PPAs**, while offering no upfront cost, often come with less obvious drawbacks. The most significant trade-off is losing eligibility for the federal tax credit and other local incentives, which go to the third-party owner, meaning you miss out on thousands of dollars in potential savings. This means your overall financial benefit is limited solely to the savings on your electricity bill, which might be further eroded by annual rate escalators. Furthermore, these agreements are long-term (20-25 years) and can be difficult to get out of, often requiring a buyout or a transfer to a new homeowner. If you sell your home, the new buyer must qualify and assume the lease, which can complicate or even jeopardize the sale, a point often highlighted in guides on choosing the best solar roofing company, as lenders can be hesitant to finance homes with existing solar agreements. Escalator clauses, where your monthly payment or per-kWh rate increases annually by a small percentage (typically 1-3%), can also significantly diminish your savings over two decades, making careful projection crucial.

Even with a **cash purchase**, while offering the best financial return, there's the opportunity cost of tying up a large sum of money that could have been invested elsewhere, a factor to weigh against your other financial goals. Additionally, the homeowner assumes all responsibility for maintenance and potential repairs, though modern solar systems are generally very reliable and often come with long warranties; it's wise to budget for potential issues or choose a reputable installer with strong post-installation support. Regardless of the method, choosing the right residential solar panel installer is paramount to mitigate risks like poor installation or inadequate system design, which can undermine the performance and savings of any system and lead to unexpected costs. What hidden clauses or unforeseen scenarios might turn your sunny solar dream into an unexpected financial burden, and how can careful planning help you avoid them?

Main points

- Understanding the core difference between solar system ownership (cash, loan) and access (lease, PPA) is fundamental to choosing the right financing path.

- Solar loans offer ownership and access to federal and local incentives, spreading the cost over time, but require a good credit score and careful review of interest rates and terms.

- Solar leases and Power Purchase Agreements (PPAs) provide immediate electricity bill savings with no upfront cost or maintenance responsibility, but forfeit ownership and most financial incentives to a third party.

- An outright cash purchase typically yields the highest long-term savings and full control over the system, allowing you to capture all available tax credits and rebates, despite the significant initial investment.

- Your best option depends on your financial situation, willingness to manage debt, desire for ownership, and local incentives, requiring a careful calculation of lifetime costs and benefits.

- Key blind spots include hidden fees and escalator clauses in contracts, the complexity of transferring leases during a home sale, and the crucial importance of a reputable installer.

- Utilizing tools like a 'solar financing loans vs lease vs cash calculator' is vital for comparing options comprehensively, factoring in specific state incentives (e.g., California, Florida), and considering real-world scenarios often discussed in community forums.

Starting your solar journey is a significant step towards a sustainable future and financial savings. By thoroughly evaluating these financing options, weighing the benefits against the risks, and consulting with trusted professionals, you can confidently choose the path that illuminates your home and your financial well-being for years to come.