Demystifying Solar Financing: Your Comprehensive Guide to Cost and Options

Navigating Loans, Leases, and Incentives for Your Residential Solar Investment

Considering solar but overwhelmed by the numbers? Understanding the actual 'Solar Financing Cost' is the first step toward energy independence.

From low-interest loans to zero-down leases, the world of solar financing offers many paths. Which one will offer the most savings for your home?

Beyond the panels, the financial structure of your solar project determines its long-term value. Are you making the most informed decision?

The dream of harnessing the sun's power for your home is more attainable than ever, but the financial journey can seem complex. Understanding 'Solar Financing Cost' goes beyond the price tag of panels; it encompasses a range of options, from outright purchase to various loan structures and third-party ownership models. This comprehensive guide will illuminate the pathways available for residential solar, breaking down typical costs, interest rates, and the critical factors that influence your final investment.

Our goal is to equip you with the knowledge needed to confidently compare different financing routes, assess their long-term implications, and ultimately choose the financial strategy that best aligns with your budget and energy goals. Prepare to explore the nuances of solar loans, leases, power purchase agreements, and the incentives designed to make solar energy a smart financial decision for your household.

Quick navigation

- Decoding the Initial Investment: What Drives Your Solar Financing Cost?

- Navigating Your Options: The Landscape of Solar Financing

- Solar Loans: Understanding Rates, Terms, and Providers

- Solar Leases and Power Purchase Agreements (PPAs): An Alternative Path

- What this means for you

- Risks, trade-offs, and blind spots

- Maximizing Your Savings: Incentives and Financial Planning

- Main points

Decoding the Initial Investment: What Drives Your Solar Financing Cost?

Before examining financing options, it's essential to understand what constitutes the overall cost of a residential solar system. This isn't just about the glossy panels on your roof; it's a complex mix of several key components. Firstly, the core hardware includes the solar panels themselves, with their efficiency and brand influencing price. Then there are the inverters, which convert the DC electricity from the panels into usable AC electricity for your home; you'll typically choose between string inverters, which are simpler and more cost-effective for uniform arrays, or microinverters, which optimize each panel individually and can be more beneficial for shaded or complex rooflines.

Battery storage, while optional, is an increasingly popular addition, providing energy independence during outages and allowing homeowners to store excess solar power for use during peak demand. This significantly adds to the upfront cost but offers substantial long-term benefits. Beyond the equipment, installation complexity plays a major role. Factors like your roof type (shingle, tile, metal), its condition, and the angle and orientation to the sun all impact labor hours. Permitting, inspection fees, and interconnection charges from your utility company are also non-negotiable elements. Finally, local labor rates and the geographical location of your home, including average sunlight hours and potential snow load considerations, will influence the system's size (measured in kilowatts or kW, based on your energy consumption) and thus the total cost. It's crucial to remember that advertised prices often represent the gross cost before any incentives or financial aid are applied, which can significantly alter your net investment. Is the upfront sticker price the true measure of your solar investment, or is there more beneath the surface?

Navigating Your Options: The Landscape of Solar Financing

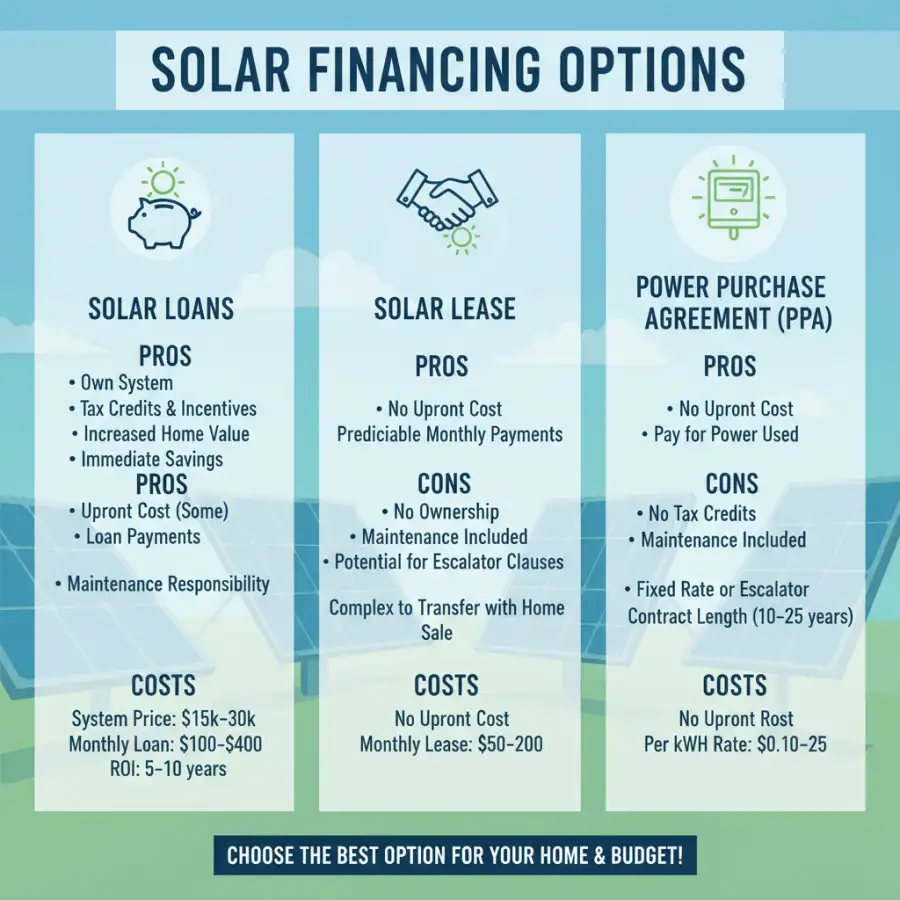

The journey to solar energy for your home doesn't have a single path; instead, it offers a diverse landscape of financing options, each with its own advantages and considerations. Broadly, these options fall into two main categories: direct ownership and third-party ownership. Direct ownership, as the name suggests, means you outright own the solar energy system. This can be achieved through a cash purchase, where you pay the full amount upfront, or through various solar loan structures, which allow you to spread the cost over time while still maintaining ownership.

On the other hand, third-party ownership models, such as solar leases and Power Purchase Agreements (PPAs), involve a solar provider owning, installing, and maintaining the system on your property. In these scenarios, you essentially "rent" the system or buy the electricity it produces, rather than owning the hardware itself. The fundamental difference lies in who claims the valuable federal and state incentives, who is responsible for maintenance, and how the overall long-term financial benefits accrue. We'll explore each of these categories in more detail, but it's important to recognize that no single option is universally superior. The "best" choice is deeply personal, depending on your financial situation, tax appetite, long-term homeownership plans, and comfort level with upfront investment versus ongoing payments. With so many paths to solar, how do you know which one truly aligns with your financial aspirations and long-term home ownership goals?

Solar Loans: Understanding Rates, Terms, and Providers

For many homeowners, a solar loan offers the ideal balance: the ability to own their solar energy system and claim all available incentives, while spreading the financial outlay over a manageable period. This approach avoids the significant upfront cash requirement of a direct purchase while still allowing you to reap the full economic benefits of solar. Solar loans come in several forms, each with distinct characteristics.

Secured solar loans are often the most attractive, typically taking the form of home equity loans (HEL) or home equity lines of credit (HELOCs). These loans use your home as collateral, which generally translates to lower interest rates (often in the 3-6% range for well-qualified borrowers) and longer repayment terms, typically 10 to 20 years. Unsecured personal loans, while usually easier and quicker to obtain, carry higher interest rates (often 7-15%) due to the lack of collateral. Additionally, many solar installers partner with specialized solar loan providers, offering tailored financing packages with competitive rates and terms designed specifically for renewable energy projects.

Typical loan terms for solar range from 10 to 25 years, with interest rates influenced by your credit score, the loan amount, and prevailing market conditions. You might encounter down payments, closing costs, and in some cases, options for interest-only periods or re-amortization. The primary financial advantage of a solar loan is that, as the system owner, you are eligible for significant federal and state incentives, most notably the Federal Solar Investment Tax Credit (ITC). This credit, currently at 30% of the system cost, can substantially reduce your net investment, making the overall 'Solar Financing Cost' much more appealing. Integrating a solar loan is a critical step in initiating a residential solar panel installation, ensuring that you have the necessary capital to move forward with the project. Are you truly getting the most competitive rate, or is there a hidden cost waiting in the fine print of your loan agreement? For more insights on the overall installation process, consider reviewing comprehensive guides on residential solar panel installation.

Solar Leases and Power Purchase Agreements (PPAs): An Alternative Path

For homeowners seeking to go solar with minimal to no upfront investment and no maintenance responsibilities, third-party ownership options like solar leases and Power Purchase Agreements (PPAs) present compelling alternatives. In both models, a solar provider, often referred to as a third-party owner (TPO), handles the entire process: they design, install, own, and maintain the solar energy system on your property. This means you avoid the direct 'Solar Financing Cost' of purchasing the equipment.

With a **solar lease**, you pay a fixed monthly 'rent' for the use of the solar system, much like leasing a car. This monthly payment is predictable and is often structured to be less than your previous average electricity bill, resulting in immediate savings. The solar provider is responsible for all maintenance, repairs, and performance guarantees, removing any hassle from your end.

A **Power Purchase Agreement (PPA)** differs slightly. Instead of paying a fixed monthly lease payment, you agree to buy the electricity generated by the panels at a predetermined per-kilowatt-hour (kWh) rate. This rate is typically lower than your utility's retail rate, guaranteeing savings from day one. Again, the provider owns and maintains the system, ensuring its optimal performance.

The primary advantages of both leases and PPAs include little to no upfront cost, immediate reductions in your electricity bills, and the complete absence of maintenance worries. However, there are trade-offs. The homeowner does not own the system, which means they cannot claim valuable federal or state solar incentives like the Investment Tax Credit (ITC) – those benefits go to the system owner (the provider). Leases and PPAs often include escalation clauses, meaning your monthly payment or per-kWh rate will increase by a small percentage (e.g., 2.9% annually) over the contract term, typically 20-25 years. Furthermore, transferring a lease or PPA can sometimes complicate the sale of your home, requiring the buyer to assume the agreement. When considering these options, thoroughly vetting the solar provider is paramount, as their reputation, service quality, and contractual terms will directly impact your long-term experience. For more on selecting a reputable installer, explore resources on choosing the best solar roofing company. Does foregoing system ownership truly mean foregoing control and the maximum long-term financial benefits?

What this means for you

Choosing the right solar financing option comes down to aligning it with your personal financial situation, risk tolerance, and long-term goals. The decision you make about your solar financing profoundly impacts your savings, home value, and overall experience with renewable energy. To help synthesize this, consider these practical scenarios:

- If you have substantial savings and prefer maximum long-term return: A cash purchase is typically your best bet. You own the system outright, claim all incentives (like the 30% Federal ITC), and enjoy the highest overall return on investment through significant electricity bill savings and increased home value.

- If you want ownership and incentives but prefer to avoid a large upfront payment: A solar loan, especially a secured one, is often ideal. You become the system owner, qualify for tax credits, and spread the cost over a decade or two, with predictable monthly payments often offset by immediate energy savings.

- If zero upfront cost and no maintenance responsibilities are your top priorities: A solar lease or PPA could be perfect. While you won't own the system or claim incentives, you'll benefit from lower electricity bills and the peace of mind that comes with the provider handling all repairs and performance.

Regardless of your chosen path, the long-term financial benefits of residential solar ownership are compelling. You'll significantly reduce or eliminate your electricity bills, hedging against future utility rate increases. Solar installations also demonstrably increase home value, appealing to eco-conscious buyers. Beyond personal gain, you contribute positively to environmental sustainability and gain a degree of energy independence. Due diligence is critical: always obtain multiple quotes from different providers, meticulously read and understand every clause in contracts, and consider consulting with a financial advisor or a specialized solar professional. A carefully planned residential solar panel installation, underpinned by the right financing strategy, is the cornerstone of long-term performance and financial returns. For detailed considerations in planning your installation, refer to guides on optimizing your residential solar panel installation. Beyond the numbers, how will solar truly enhance your home's value and your financial stability in the coming decades?

Risks, trade-offs, and blind spots

While the allure of solar energy is strong, ignoring the potential pitfalls and less obvious considerations in solar financing can turn a promising investment into a headache. It's crucial to look beyond the headline numbers and examine the fine print of any agreement. Hidden fees are a common pitfall. Loan origination fees, dealer fees, and other administrative charges can often be rolled into the principal of a solar loan, increasing the total amount you finance and, consequently, your overall 'Solar Financing Cost'. For leases and PPAs, be wary of early termination fees if you need to end the contract prematurely, and clarify who bears the cost of system decommissioning at the end of the term.

If you opt for a variable-rate solar loan, **interest rate fluctuations** pose a genuine risk. While initially attractive, rising interest rates over the loan's lifetime can erode your projected energy savings, diminishing the financial benefits. Another significant consideration is the **impact on home resale**. An outright owned solar system is generally seen as a valuable asset that increases your home's market value. However, transferring a solar lease or PPA can complicate selling your home, as prospective buyers must agree to assume the existing contract, which some may find unattractive or confusing.

Understanding **performance guarantees** is also vital. What happens if your system doesn't produce the promised amount of electricity? Clarify the terms of any guarantees and the recourse available. Similarly, clarify **warranty considerations**: who is responsible for the panels, inverters, and the installation itself? Is it the homeowner, the installer, or the third-party provider? These details dictate your responsibility and protection if issues arise. Ultimately, it's crucial to understand the 'true cost of ownership' over the system's entire lifespan – typically 25+ years. Don't just focus on the initial quote; consider all ongoing costs, potential fees, and the impact of inflation and interest. What are the unseen pitfalls in your solar financing journey, and how can careful planning help you avoid them?

Maximizing Your Savings: Incentives and Financial Planning

To significantly reduce your overall solar financing cost and accelerate your return on investment, it's critical to understand and utilize available incentives. These programs, offered at federal, state, and local levels, are designed to make solar energy more accessible and financially attractive.

The cornerstone of federal support is the **Federal Solar Investment Tax Credit (ITC)**. This powerful incentive allows homeowners to claim a percentage of the total cost of their solar system as a credit against their federal income taxes. Currently set at 30% for systems installed through 2032, it represents a substantial reduction in your net cost. Eligibility and claiming procedures are straightforward but require careful attention during tax season, typically with IRS Form 5695.

Beyond the federal level, a patchwork of **state and local incentives** can further enhance your savings. These vary widely by location but can include state tax credits, direct cash rebates, property tax exemptions (preventing your property taxes from increasing due to the added value of solar), and sales tax exemptions on solar equipment. Another valuable incentive is **Solar Renewable Energy Credits (SRECs)**, which allow homeowners in some states to earn credits for the clean electricity their system generates, which can then be sold on a market. Furthermore, favorable **net metering policies** allow you to sell excess electricity back to the grid, often at retail rates, providing credits on your utility bill.

It's essential to research and understand all available incentives *before* finalizing any financing decision or signing a contract. These incentives can dramatically alter the net cost of your system and thus the most financially advantageous path. Effective financial planning around solar involves more than just selecting a loan or lease. Budget for any potential out-of-pocket expenses, understand the tax implications of the ITC and any other credits, and forecast your energy savings over the 25-30 year lifespan of your system. This holistic approach ensures you maximize your financial benefits. Are you leaving money on the table by not fully understanding the comprehensive suite of available solar incentives?

Main points

- Solar financing costs are driven by system components (panels, inverters, batteries), installation complexity, and labor.

- Financing options include direct ownership (cash, solar loans) and third-party ownership (leases, PPAs), each with distinct benefits and drawbacks.

- Solar loans enable system ownership and eligibility for incentives, with rates varying by credit and loan type.

- Leases and PPAs offer low upfront costs and no maintenance, but the homeowner doesn't claim incentives.

- Choosing the right financing path depends on your financial situation, willingness for upfront investment, and long-term goals.

- Be aware of hidden fees, interest rate fluctuations, resale impacts, and warranty details when evaluating options.

- Federal, state, and local incentives, particularly the 30% ITC, are crucial for reducing net costs and maximizing savings.

Understanding the nuances of solar financing is key to making an informed decision for your home. We encourage you to research thoroughly, gather multiple quotes, and consult with financial advisors or solar professionals to confidently choose the best financial path for your sustainable energy future.